1. What is the Goat Milk Market and why is it significant?

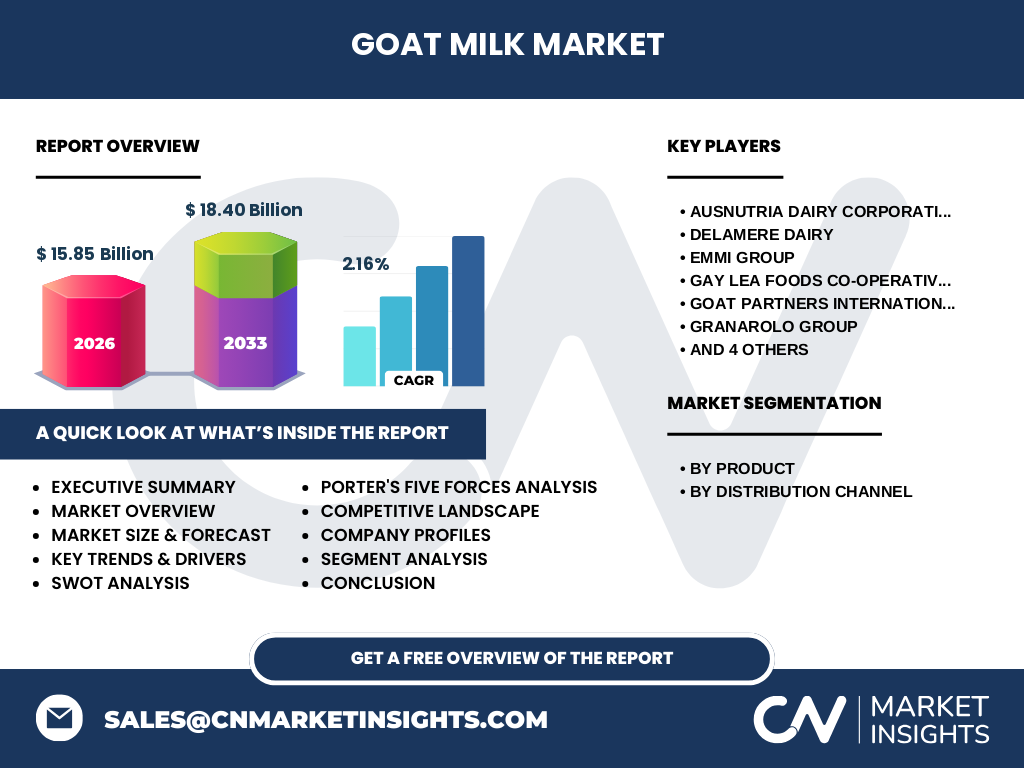

The Goat Milk Market comprises the production, processing, and distribution of goat-derived dairy products, including liquid milk, cheese, and milk powder. It spans a global supply chain from goat farms to retail channels such as hypermarkets, specialty stores, and online platforms. The market’s significance stems from growing consumer preference for nutritious, digestible dairy alternatives, the rising prevalence of lactose intolerance, and the expanding demand for premium functional foods. With a 2026 valuation of 15.85 billion USD, the sector represents a robust segment of the broader dairy industry, offering opportunities for producers, processors, and retailers seeking differentiation.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Goat Milk Market?

Key drivers include increasing health awareness, the perception of goat milk as a low‑fat, high‑protein option, and its suitability for specialty diets. Urbanisation and rising disposable incomes in emerging economies further boost demand for premium dairy. Restraints involve limited goat herd density in some regions, higher production costs compared to cow milk, and regulatory barriers concerning labeling. Challenges revolve around supply chain logistics, especially maintaining product freshness across long distances, and educating consumers about shelf‑stable formats like milk powder. Opportunities arise from product innovation (flavoured cheeses, fortified powders), expansion of e‑commerce channels, and the potential to tap into niche markets such as infant nutrition and sports nutrition.

3. Which trends are currently influencing the Goat Milk Market?

Current trends include the surge in “clean‑label” products, prompting manufacturers to highlight natural sourcing and minimal processing. Plant‑based alternatives have indirectly driven interest in animal‑derived specialty milks, positioning goat milk as a “better‑for‑you” option. The rise of functional nutrition—adding probiotics, omega‑3s, and vitamins to goat milk products—is gaining traction. Additionally, there is a noticeable shift toward sustainability, with farms adopting regenerative grazing practices to appeal to eco‑conscious consumers. Lastly, digital marketing and direct‑to‑consumer online sales are reshaping distribution, especially for niche cheeses and premium milk powders.

4. How did COVID‑19 affect the Goat Milk Market and what is the recovery outlook?

During the pandemic, disruptions in logistics and temporary closures of specialty retail outlets slowed sales, while heightened health concerns spurred interest in immune‑supporting foods, partially offsetting the dip. Online channels experienced accelerated growth, compensating for reduced foot traffic in supermarkets. Post‑2021, the market has shown a steady rebound, supported by the reopening of hospitality venues and a renewed focus on health‑centric diets. The recovery trajectory aligns with the overall CAGR of 2.16 % projected through 2033, indicating a resilient market that is adapting to new consumer behaviours.

5. Who are the major competitors and how consolidated is the Goat Milk Market?

Key players include Ausnutria Dairy Corporation Ltd., Delamere Dairy, Emmi Group, Gay Lea Foods Co‑operative Ltd., Goat Partners International, Inc., Granarolo Group, Hay Dairies Pte Ltd., Kavli, Stickney Hill Dairy, Inc., and Summer Hill Goat Dairy. The competitive landscape is moderately fragmented, with several midsized firms operating in distinct geographic niches. While no single entity dominates globally, strategic alliances and acquisitions are emerging as consolidation tools, allowing companies to broaden their product portfolios and extend distribution reach, especially in high‑growth regions.

6. What are the high‑level insights and key findings from the Goat Milk Market research?

The market stands at 15.85 billion USD in 2026 and is projected to reach 18.40 billion USD by 2033, reflecting a stable CAGR of 2.16 %. Growth is propelled by health‑driven demand, product diversification, and channel expansion, particularly online. Regional analysis reveals strong performance in Europe and North America, while emerging markets in Asia‑Pacific show increasing adoption driven by rising incomes. Competitive dynamics are shaped by innovation in value‑added products and strategic partnerships that enhance market penetration. Overall, the sector offers a compelling investment narrative anchored by steady demand and untapped growth pockets.

7. What are the forecast expectations for the Goat Milk Market from 2025 to 2032?

Building on the 2026 baseline, the market is expected to expand to roughly 18.40 billion USD by 2033, maintaining an annual growth rate of 2.16 %. The forecast indicates gradual but consistent expansion across all product categories—milk, cheese, and milk powder—with the greatest upside anticipated in the premium cheese segment and fortified milk powders targeting health‑focused consumers. The forecast also anticipates a continued shift toward digital sales channels, which are projected to capture a growing share of total revenue.

8. How is the Goat Milk Market sized and shared across product and distribution segments?

Segmentation by product includes Milk, Cheese, and Milk Powder, each contributing to the overall market value. While exact share percentages are not disclosed, all three categories benefit from the projected CAGR, with cheese often commanding higher margins due to artisanal positioning, and milk powder gaining traction for its longer shelf life and suitability for export. Distribution channels are split among Hypermarkets and Supermarkets, Convenience Stores, Specialty Stores, and Online platforms. The online segment has recorded the fastest growth rate, reflecting changing shopper habits, whereas hypermarkets continue to provide the largest volume base.

9. What is the geographic distribution of the global Goat Milk Market?

The global market is spread across major regions, with Europe and North America representing the largest consumption hubs due to established dairy cultures and higher per‑capita goat milk intake. Asia‑Pacific is emerging as a significant growth engine, driven by expanding middle‑class populations and growing awareness of goat milk’s nutritional benefits. Latin America and the Middle East contribute niche demand, primarily through specialty stores and expatriate communities.

10. How does the Goat Milk Market perform in each major region?

In Europe, mature consumer bases and strong artisanal cheese traditions sustain robust sales, particularly for premium cheeses. North America shows steady growth in liquid goat milk and flavored milk powders, aided by health‑focused retail chains. Asia‑Pacific’s performance is buoyed by increasing urbanisation and a willingness to adopt alternative dairy products, with online sales accelerating market entry. Latin America experiences modest growth, largely confined to specialty stores, while the Middle East’s demand is driven by expatriate populations and high‑end retail outlets.

11. Which companies lead the Goat Milk Market and what are their strategic approaches?

Leading firms such as Ausnutria Dairy Corporation Ltd. and Emmi Group focus on product diversification, launching fortified milk powders and value‑added cheeses. Delamere Dairy and Summer Hill Goat Dairy emphasize sustainable farming and traceability, leveraging consumer trust. Granarolo Group and Kavli pursue geographic expansion through strategic partnerships, especially in emerging Asian markets. Goat Partners International, Inc. and Hay Dairies Pte Ltd. concentrate on niche premium offerings and direct‑to‑consumer channels, reinforcing brand loyalty.

12. How do Porter’s Five Forces shape the Goat Milk Market?

Threat of New Entrants: Moderate, due to high capital requirements for herd development and processing facilities. Bargaining Power of Suppliers: Relatively high, as quality goat milk depends on limited herd resources and specialized breeding. Bargaining Power of Buyers: Growing, especially through online platforms that enable price comparison. Threat of Substitutes: Significant, with plant‑based milks competing for health‑conscious consumers. Industry Rivalry: Intense, driven by product innovation, brand differentiation, and regional expansion strategies.

13. What are the SWOT highlights for the Goat Milk Market?

Strengths: Nutritional advantages, premium positioning, and expanding product formats.

Weaknesses: Higher production costs and limited herd scalability.

Opportunities: Functional fortification, e‑commerce growth, and entry into emerging markets.

Threats: Plant‑based alternatives, regulatory hurdles, and supply chain disruptions.

14. How does the value chain of the Goat Milk Market operate?

The value chain begins with goat farming, where genetics, nutrition, and animal welfare determine milk quality. Milk collection and primary processing (pasteurisation, standardisation) follow, leading to secondary processing into cheese or powder. Packaging and cold‑chain logistics ensure product integrity, after which distribution occurs via hypermarkets, specialty stores, or online retailers. Finally, marketing and consumer education complete the chain, influencing demand and brand perception.

15. What investment insights can be drawn from the Goat Milk Market?

Investors should focus on companies that are expanding into functional milk powders and premium cheese lines, as these segments exhibit higher margin potential. Firms with strong e‑commerce capabilities are positioned to capture the fastest‑growing distribution channel. Additionally, partnerships that secure sustainable goat herd supplies can mitigate raw‑material risk. Allocating capital toward firms entering high‑growth regions like Asia‑Pacific offers upside, especially when combined with localized branding and regulatory compliance.

16. What are the concluding takeaways from the Goat Milk Market analysis?

The Goat Milk Market is on a solid growth path, projected to reach 18.40 billion USD by 2033 with a steady CAGR of 2.16 %. Health‑focused consumer trends, product innovation, and digital distribution are the primary engines of expansion. While supply constraints and competition from plant‑based milks pose challenges, opportunities in functional fortification and emerging markets present compelling avenues for growth. Stakeholders that prioritize sustainability, brand differentiation, and omnichannel reach will likely lead the market forward.

17. Which research methods were employed to compile this Goat Milk Market report?

The study combined primary interviews with industry executives, farm owners, and retail buyers, alongside secondary analysis of company filings, trade publications, and government statistics. Market sizing utilized a top‑down approach based on the provided 2026 valuation, while forecasting applied compound annual growth rate extrapolation. Competitive assessment integrated SWOT and Porter’s Five Forces frameworks, and regional analysis drew on publicly available import‑export data and consumer surveys.

18. What is the scope of this Goat Milk Market research?

The scope covers global production, processing, and distribution of goat milk, cheese, and milk powder across all major retail channels. It includes quantitative market sizing, qualitative trend assessment, competitive landscape, and strategic insights for the 2025‑2032 horizon. The study excludes unrelated dairy segments such as goat meat and non‑dairy alternatives, focusing solely on the defined product and channel categories.

19. Which key companies have announced recent developments in the Goat Milk Market?

Ausnutria Dairy Corporation Ltd. recently launched a fortified goat milk powder line targeting the infant segment. Emmi Group announced a partnership with a leading European specialty retailer to expand its artisanal goat cheese portfolio. Granarolo Group reported the acquisition of a small‑scale goat farm in Italy to secure raw‑material supply. Hay Dairies Pte Ltd. introduced a direct‑to‑consumer subscription service for premium goat milk delivered online. These initiatives illustrate the industry’s focus on product innovation, supply chain integration, and digital engagement.